20 April 2018

20 April 2018With capital becoming globalised, international investors look for the minutest of opportunities across the world to improve return on their funds. Such endeavours, many a time, fall into the grey zone where the difference between legal and illegal becomes very thin. Two such grey zone cases refer to ‘treaty shopping’ and ‘round tripping’.

To simplify, suppose there is an investor in country A, who wants to invest in country B. Instead of investing directly from country A to B, the investor tries to look for a country C which has a tax treaty with B.

The objective is to find a tax treaty that can be used to lower the tax payable on the income arising from that investment. Then the investor would route the investment to B through this third country C. This process of routing investment/capital flows through a third country only to take the benefits of tax treaties of that country is called treaty shopping.

An extreme case of treaty shopping arises when it is used by domestic investors. In these cases, which are referred to as round tripping, a domestic investor of country B would first take his/her funds to country C and establish a shell company there so as to acquire the legal identity as a resident of country C. Then the investor would bring the money back to country B disguised as foreign investment and thus be able to take advantage of the benefits available to investors from country C. By engaging in practices such as treaty shopping and round tripping, many investors and firms are able to escape paying their fair share of taxes, which results in loss of valuable tax revenue for governments.

The Centre for Budget and Governance Accountability (CBGA), a New Delhi-based think tank, recently did a study focusing on FDI inflows to India between 2004 and 2014. The study makes use of a dataset which identifies the real home country of investors for the investment inflows coming to India on the basis of where their headquarters are based. By comparing where the investor is actually based versus where the investment is reported to come from in the official data, this report identifies if a particular investment flow is coming directly from the investor’s home country or is being routed through a third country in order to exploit the tax benefits.

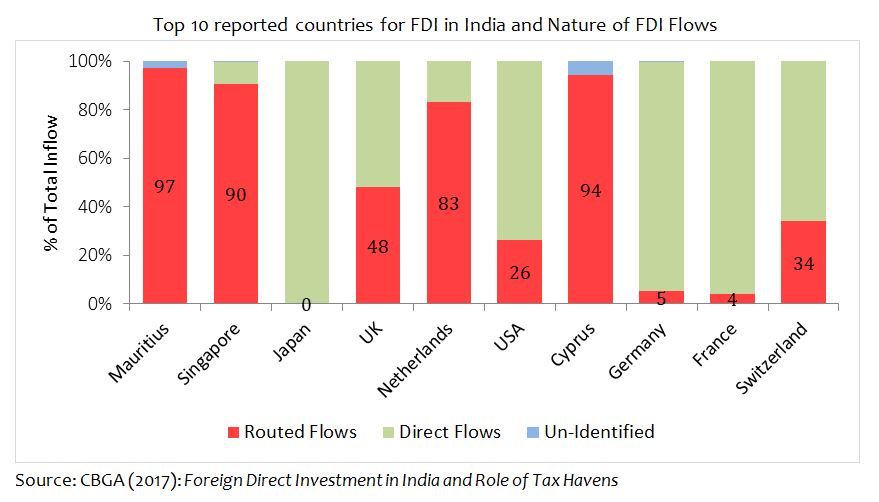

The following chart highlights that for the top ten countries reported in the official data as the largest source of FDI in India, how much of the investment is actually by the investors from that country, and how much is merely being routed through that country by investors based in some other country.

The study shows that many countries like Mauritius, Singapore and Cyprus were being used to route capital flows from other countries.

In fact, Mauritius and Singapore, reported in the official statistics as the two largest source of FDI in India, along with Cyprus, have long been suspected to aid treaty shopping and round tripping. The above chart confirms this suspicion to a certain extent by providing a quantitative estimate of the extent of routed capital flows. In the case of Mauritius and Cyprus, almost all of the identified flows are in fact routed, while in the case of Singapore this touches 90%.

To understand the motivations behind an investor’s decision to route his/her investment through a particular country, the study analyses India’s double taxation avoidance agreements (DTAAs) with the above countries. DTAAs are essentially the regulations which determine that in case of a cross-border investment, which of the two countries will have taxing rights on the investment and at what rate.

The rationale behind this analysis of DTAAs was to find if investments coming to India from one country have favourable tax benefits compared to investments from other countries. The study found that investments coming from Mauritius, Singapore and Cyprus enjoyed ‘effective zero tax rate on capital gains’, which was not available to investments from other countries.

For example – according to the India-Mauritius DTAA signed in 1983, capital gains tax rights on the investments in India by Mauritius residents were granted to Mauritius. However, there are no capital gains taxes in Mauritius, effectively meaning a Mauritian investor didn’t have to pay any capital gains taxes on the investments made in India, leading to a zero effective capital gains tax. This ‘zero capital gains tax rate’ made Mauritius a popular choice for investors worldwide to route their investments into India. Investors from other countries would first send funds to Mauritius, take the identity as a Mauritian resident and then invest from Mauritius to India.

This process of routing investment made Mauritius, a country with a population of 13 lakh and annual GDP of $12 billion, the largest source of FDI in India with close to 35% share in the last 15 years, much ahead of other heavyweights like the US, UK and Japan.

The method became so popular that it earned its own nomenclature as ‘Mauritius route’, encompassing other jurisdictions like Singapore and Cyprus. Both these countries too had zero effective capital gains taxes and were also used to facilitate routed funds to India. The DTAAs with above countries made it beneficial not only for foreign investors to route funds through them; they even made it beneficial for the domestic investors to engage in round tripping.

Since this process of routing investment also had negative implications for the government tax revenue, the Indian government has been trying to amend the DTAAs with the above three countries. After years of negotiation, in 2016 India finally managed to amend the DTAAs with Mauritius, Singapore and Cyprus, and removed the zero effective tax rates for capital gains.

According to the amended treaty, the preferential tax benefits will be partially removed from FY’2017, and will be removed completely from FY’2019.

These amendments were widely reported in the media and many commentators described it as the end of treaty shopping and round tripping.

The rise of Netherlands

However, the CBGA study finds that apart from the above three countries, there are DTAAs with other countries which still offer a beneficial tax regime to its investors investing in India, such as Netherlands, Spain and France.

The DTAA with Netherlands has benefits similar to the earlier Mauritius treaty in relation to capital gains tax, after fulfilling certain conditions. The existence and continuation of these DTAAs opens up the possibility that these countries may turn out to be the new Mauritius route.

In fact, the latest official statistics for FDI inflows to India show that during the period January-December 2017, Netherlands has already reached number three in the list of largest FDI contributors to India, just behind Mauritius and Singapore. Industry reports are also indicating that international investors are looking at these countries to route future investments to India.

It took more than a decade and multiple rounds of negotiations with the above three countries to amend the DTAAs. It is hoped that the government of India will do well by proactively looking to plug loopholes in the other existing DTAAs, and avoid the creation of new Mauritius routes.